February is the month of love, and although Valentine’s Day is over, your love for those close to you never stop. The act of insuring your love with Life Insurance is no better way to protect your loved ones and show them you how you feel. It can provide security when those left behind need financial help the most. “There are no guarantees. You have to prepare for those ‘what ifs.’” Lifehappens.org presents Real Life Stories. These are True Love Stories that illustrates why it’s so important for people to include life insurance in their financial plans. These families highlighted in these stories could have anticipated the challenges they’d face.

Think!! How would you and your family manage financially if faced with similar challenges!

Stephen Miller: Protecting the Future

A mutual friend with a new dog brought Stephen and Katie together. Stephen had headed to his friend’s house to meet the new furry member of the family, and when he got there, he saw Katie playing with dog in the backyard. “Katie was so outgoing,” says Stephen. “She was the nicest person you’ll ever meet.”

That first meeting led to beach outings and concerts, and over time to getting married and thinking about starting a family.

It was Katie who suggested they get life insurance. Stephen admits he wasn’t too happy about the idea. They were young and healthy, so he didn’t see the point. Katie, however, convinced him to sit down with insurance professional Rose Goheen, who walked them through the process and presented them with affordable options. They both decided to get life insurance coverage.

When the couple welcomed Chase, they decided to reevaluate their life insurance. Given their expanding family and responsibilities, they both bought additional life insurance. It was during her recovery from giving birth to Reid that Katie realized something was wrong. Her doctor confirmed her suspicion that the abdominal lump she felt was something much more serious. In fact, it was an aggressive form of cancer.

Katie, with the love and support of her family, valiantly fought the disease, but just over a year later it claimed this young mom’s life. She was just 30.

Michael, 32, was a fit and healthy family man. As he left to run a 10K race, he kissed his wife, Traci, good-bye along with newborn Calvin and “big” sister Josie. He never made it home. As he crossed the finish line, Michael collapsed and died. The Kovacic family would never be the same.

Thankfully, they had life insurance. Even though the young couple had been living paycheck to paycheck, their insurance professional had convinced them to buy an affordable policy.

Traci says the hardest part for her was knowing that the love of her life was never coming home. “But the reality is that everything else stayed the same,” she says. “The paychecks stopped immediately, but I still had to keep the lights on, buy food, pay the mortgage and take care of the kids. Having life insurance meant I didn’t have to make any immediate decisions or sell the house.”

“The life insurance saved us—and it still does today,” she says.

Jenny was single and in her 20s, but that didn’t mean she wasn’t thinking about the future. In fact, she knew she wanted to have a family one day and that saving for retirement—even this early on—was a priority.

That’s why after meeting with insurance professional Jim Silbernagel, she decided to buy a permanent life insurance policy. She knew it would help her with both goals: provide the life insurance coverage she sought and the ability to accumulate cash value to help with saving for retirement.

Jenny’s dream of having a family did come true. She met Jim on a blind date, and once married, they welcomed a son, Michael, and then several years later twins, Samuel and Nathaniel. As often happens with growing families, finances got stretched tight, and Jim suggested they cancel Jenny’s policy to save money. Jenny was adamant that they keep it. Instead, they used some of the accumulated cash value to pay the premium and keep the policy in force.* That decision would be life changing for her family.

The Chich family was looking forward to welcoming their fourth child—a girl, but tragically Jenny died while giving birth. The shock to her family was overwhelming. While life insurance could never replace their vibrant wife and mother, Jim says that Jenny’s policy helped the family in the aftermath of her death. He was able to take a yearlong leave of absence from his job to care for newborn Emma and the boys, who were all younger than 6. “I was able to focus on my kids and not worry about how I was going to buy a gallon of milk,” says Jim.

_______________________________________

You may not always be there for your loved ones but you can always take care of them. These Life Insurance Love Stories are examples of the benefits a policy will serve if an unexpected or tragedy occurs, and you know your loved ones will not bear a financial burden in addition to the loss they feel.

If you’d like more information on life insurance or would like to purchase a new life insurance policy, I can help. Kelly Burke Insurance represents the brand-name insurance companies you know and trust. Contact us at (708) 444-0050 or kelly@kellyburkeinsurance.com

We all know that living in Illinois we can experience temperatures and wind chills that are below -20. Our heating systems are not designed for. -20º to -30º temperatures with wind chills down to -50º, and can create a lot of damage to your house.

Homes can struggle to keep up, and the temperature may drop while the heating system is working at full capacity. To help your home make it through the winter without any mishaps, here are tips to properly winterize your home, inside and outside.

Inside The House

Keep your house heated to a minimum of 65 degrees. The temperature inside the walls where the pipes are located is substantially colder than the walls themselves. A temperature lower than 65 degrees might not keep the inside walls from freezing.

Identify the location for the main water shutoff in your home. Find out how it works in case you have to use it.

Open hot and cold faucets enough to let them drip slowly. Keeping water moving within the pipes will prevent freezing.

If you use fireplaces, wood stoves and electric heaters, watch them closely and make sure they are working properly.

Remember to close the flue in your fireplace when you’re not using it.

When traveling, ask a neighbor to check the house regularly. If there is a problem with frozen pipes or water leakage, attending to it quickly could mean far less damage.

If you plan to be away for an extended period of time, have the water system, including pool plumbing, drained by a professional to keep pipes from freezing or bursting.

Outside The House

Keep sidewalks and entrances to your home free from snow and ice.

Watch for ice dams near gutter downspouts. Ice dams can cause water to build up and seep into your house.

Clear gutters of leaves and debris to allow runoff from melting snow and ice to flow freely.

If you own a swimming pool and temperatures are expected to dip below freezing, run the pool pump at night to keep the water flowing through the pipes.

Make sure all hoses are disconnected from outside spigots.

If your garage is attached to your house, keep the garage doors closed. The door leading to the house is probably not as well-insulated as an exterior door.

If ice forms on tree limbs, watch for dead, damaged or dangerous branches that could break loose when stressed by ice, snow or wind and damage your house or car, or injure someone on or near your property.

If your home suffers water damage, it is important to make sure that it is properly dried and repaired to prevent any potential problem with mold. Remember, mold cannot survive without moisture.

Frozen or Burst Pipes

If you discover that pipes are frozen, don’t wait for them to burst. Take measures to thaw them immediately, or call a plumber for assistance.

If your pipes burst, first turn off the water and then mop up spills to avoid further damage.

Your Insurance Coverage

Standard homeowners policies will cover most kinds of damage that result from a freeze. For instance, if house pipes freeze and burst or if ice forms in gutters and causes water to back up under roof shingles and seep into the house. You would also be covered if the weight of snow or ice damages your house.

Most policies do not cover backups in sewers and drains or flood damage, which can also happen in winter. To be covered for flooding, you need a separate flood policy from the National Flood Insurance Program.

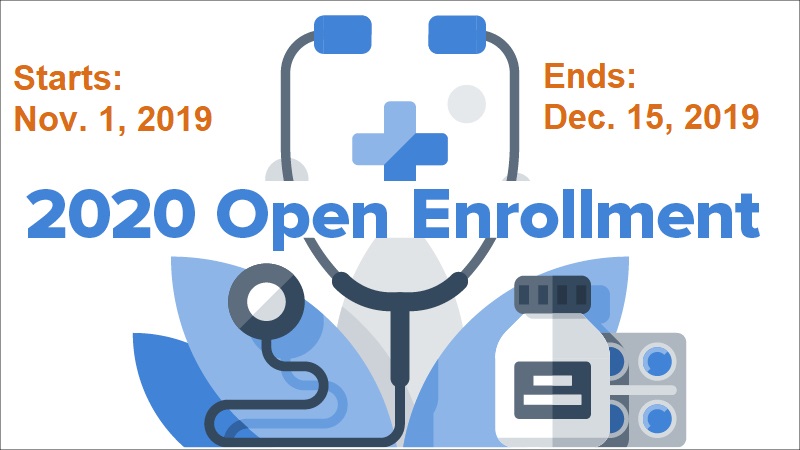

It’s time for Medicare Fall Open Enrollment. Knowing how to navigate coverage options and understanding what changes are in store for Medicare in 2020 will help you make the most informed decisions during Fall Open Enrollment.

During this time, you can make changes to your prescription drug plan, enroll in a plan, change your Medicare Advantage Plan, or enroll in a Medicare Advantage Plan.

WHO IS ELIGIBLE FOR MEDICARE? People that are 65 or older or those that have been disabled and collecting social security disability for 24 months.

What to Expect in 2020

Plan F will no longer be offered to newly eligible enrollees. If you have a Plan F currently, your plan will remain the same. If you became eligible for Medicare before January 1, 2020 you will still be able to enroll in Plan F.

Humana had made a change to their prescription drug plan. Those on the Humana Walmart Plan have been re-mapped to the Humana Premier RX plan. Humana is offering a less expensive option, but we MUST make sure your drugs are covered in the new plan. If you want to discuss your options, please have your list of drugs available.

The Part D (prescription drug) deductible has increased to $435. Many carriers offer plan with $0 deductible for drugs in Tier 1 or Tier 2.

Donut Hole: The initial limit has increased to $4,020.

United Healthcare/AARP and Blue Cross Blue Shield have little to no changes to their plans for 2020. If you are happy with your plan, the plan will automatically renew.

Tips to Reducing Your Medicare Premium

Consider a Medicare Advantage Plan. If you are already in one, you may want to consider another carrier. Be sure to pick a plan with a maximum out of pocket and confirm that your doctors accept the plan before switching. This will protect you in the event of a “bad” year.

Consider switching the type of Supplemental Plan you are in currently (i.e. Plan G is often less expensive than a Plan F). I will caution, changing your plan may require you to pay for services that you have not paid for in the past. For example, a Plan N will charge the $185 deductible and $20 co-pay for doctors’ visits.

Review your drug lists with other carriers. Medicare.gov is a great source for reviewing rates with other carriers. Simply plug in your drug information, select your pharmacy, and review the different plans available (based on the drugs you are taking).

Consider switching pharmacies. First, watch to make sure your pharmacy is still in the Preferred Network with your prescription drug plan. Second, find out what the different pharmacies charge for your drugs. You may see a difference that can save you some time in reaching the donut hole.

This is an extremely busy time for me. I suggest scheduling early as my schedule will fill up. Contact me at 708-444-0050 or kelly@kellyburkeinsurance.com.

Please include your availability (i.e. mornings, afternoons, or evenings) and the type of appointment you are requesting (face to face or conference call).

Open enrollment 2020 is right around the corner. That means it’s time to check in with me about your health insurance status. While we’re still in 2019, it helps to be proactive to get prepared, know the dates-and plan.

During this time, individual policy holders can enroll in a health plan or make changes to their existing plan. *If you obtain health insurance from your employer, you are likely to have a different Open Enrollment period.*

Whether you’re buying for an individual or a family, here’s everything you need to know about open enrollment 2020.

The penalty has been removed! This means you will no longer receive a penalty for not having coverage or for obtaining a plan that does not meet the requirements of The Affordable Care Act (i.e. Short-Term Medical Plans).

Each carrier will continue to offer virtual visits. Policy holders can call or chat online with a nurse practitioner to obtain a diagnosis and prescription for medication. There is a small co-pay or $0 co-pay for this service (depending on the carrier and plan).

Group plans are still an option for small employers. Blue Cross Blue Shield does offer relaxed guidelines during this time to allow for a 1-person group. The employer must have at least 2 full time employees that are not husband and wife. This includes 1099’d employees (NEW this year).

As carriers continue to decrease or eliminate commissions to agents, I am forced to charge a fee for 2020. The fee will only be charged to Affordable Care Act Plans. This does NOT include Medicare or Short-Term Medical plans.

Short Term Medical plans will NOT offer a 12-month plan period this year. The maximum policy period is 6 months. As a reminder, these plans to not provide coverage for pre-existing conditions, maternity, or wellness visits. However, these plans are a fraction of the cost of plans offered through the Marketplace and they all have a PPO network.

Those that received a subsidy (aka assistance/reduced premium) are NOT obligated to update their income through the Marketplace. This will automatically renew based on income generated from your 2017 taxes.

AND, The Good News. There will be little to no premium increase.

How to Avoid Rate Increases

Be prepared to discuss your household, estimated adjusted gross income for 2020. This will be used to determine if you qualify for assistance.

If you are going to opt to self-insure, protect yourself with a short-term medical plan or an accident/critical illness plan. The plan works separate from health insurance and pays you based on a diagnosis of a critical illness (cancer, heart attack, or stroke) and in the event of an accident (slip, fall, and break an ankle) the plan will pay you a certain dollar amount. The purpose is to use the funds to pay towards the unexpected hospital or urgent care visit.

Review ALL of your insurance policies. I specialize in personal lines insurance, which includes auto, home and Medicare. As a broker, I have access to multiple carriers which allows me the opportunity to find the best plan based on your needs. I’ve saved people thousands by reviewing rates with multiple carriers.

This is an extremely busy time for me. I suggest scheduling early as my schedule will fill up. Contact me at 708-444-0050 or kelly@kellyburkeinsurance.com.

Please include your availability (i.e. mornings, afternoons, or evenings) and the type of appointment you are requesting (face to face or conference call).

Insurance is there for you when you need it. It’s your the safety net. But when something happens to your house or car, it can cause a lot of stress not knowing what is covered or how to file a claim. Depending on what kind of damage you’re facing, filing an insurance claim might help relieve some of the financial problems.

What Is an Insurance Claim?

Filing an insurance claim means you’re making a formal request to your insurance company to receive funds to help you pay for repairs and other expenses caused by an event (car accident or a home burglary) that is covered by your insurance.

Every situation is different, and as an Independent Agent, I can help you outline the specifics and assist in filing a claim. Below, I have provided common questions and answers to help you understand filing insurance claims forhome or auto insurance.

Insurance Claims-AUTO

Q. What I am in a car accident and not at fault?

Be sure to obtain the other person’s insurance card. Taking a picture with your phone is the easiest and most acceptable.

File the claim with the other party’s insurance carrier. If you file it with your own, you will be obligated to pay your deductible (typically $500). Your carrier will fight to get this back, however depending on the other party’s carrier (i.e. substandard) this could take months to get your money back. Once the money is returned to the carrier, they will send it back to you. This is often referred to as subrogation.

If you file with the claim with other party, you will be able to obtain a rental car at the expense of the other insurance carrier.

Do NOT wait for the other driver to file the claim. If you want to get the ball rolling, use the information from the ID card they provided to file the claim. The carrier will require a statement from you and the other driver.

Q. What if I am in a car accident and at fault?

Provide the other party with your ID card. If your car is damaged and you want it fixed, contact your carrier. If not, you can choose to pay the damages out of pocket or file it with your insurance carrier. I recommend NOT providing your ID card if you plan on paying it out of pocket. Any time you contact the carrier direct to ask about a claim or file the claim, only to pay it out of pocket, the claim will be on your record for 5 years.

If you are at fault, rental car reimbursement is only provided if you have rental reimbursement on your policy. Many people with liability only coverage or more vehicles than drivers do NOT have rental reimbursement. If this is important to you, may sure your policy covers it. The additional is cost is normally $30 per year per vehicle.

Q. What if I need rental car coverage?

Rental car reimbursement only provides coverage when your vehicle is damaged due to an accident. It does NOT provide coverage due to your vehicle breaking down.

The car rental company will ask if you want to purchase their insurance coverage. Please note, your policy will provide coverage to the rental vehicle. If you had to file a claim, the claim will be listed on your record and may affect your rate in the future.

Q. What if I am injured in a auto accident?

If you are injured in an auto mobile accident, the carrier (yours or the other party’s, depending who is at fault), will pay for medical damages, lost wages, etc. I recommend contacting an attorney to help you through the process. If you do not have an attorney, I am happy to recommend one as I work with multiple.

If the other party’s coverage does not provide enough coverage, your policy will cover for any additional expenses, under your uninsured/underinsured motorist coverage.

Insurance Claims-HOME

Q. What if I have water damage?

If the damage is caused by water, take many pictures, and get the water out ASAP. The longer the water sits, the more damage will incur, and many policies have a limit on water damage (i.e. $5,000 or $10,000).

The carrier will provide you a check for the initial damages, less depreciation. Once the damages have been repaired you must show proof to receive 100% of the payout. Receipts or construction contracts will work as proof.

Q. What if I have a claim on a rental property?

If the claim is on a rental property, the carrier will ask for proof that the property was/is occupied. If the property is insured as tenant occupied and is actually vacant, they will deny coverage. Call me if your property is vacant as we will adjust coverage immediately.

Q. What if someone is injured on my property?

If someone is injured on your property, they will receive payout from your medical coverages (typically $5,000 max) if it is worse than that they will sue you for the limit of your liability coverage/umbrella. This limit is typically $300,000 for a single-family residence and an additional $1 million with the umbrella.

Liability coverage protects you in the event anyone is injured on your property. Invited or not, you can and will be sued due to an injury.

Q. What if I have fire damage?

In the event of a fire loss, the carrier will ask for a list of ALL of your personal possessions. If it is not a total loss, they will be able to obtain pictures of the remaining items, but I ALWAYS recommend taking pictures/videos of your personal possessions; open drawers, closets, under beds, etc. You will NEVER remember everything you own without some sort of documentation.

Q. What if I need replacement costs for personal possessions?

I write ALL of my home/renters’ policies to include replacement cost of your personal possessions. This means the carrier will provide you the full value to replace your personal effects.

Q. What if my dog bites someone?

Your home/renter’s policy does provide coverage for dog bites. Depending on the severity of the dog bite, the medical portion will pay out first (typically $5,000 limit) followed by your liability (typically $300,000) and umbrella (if you have one). However, depending on the type of dog you own (Pit Bull, Rottweilers, Doberman Pinchers, etc.) the carrier may deny coverage.

If you have questions about how to file a claim or wonder if you should file a claim feel free to call me at 708-444-0050. I normally recommend you obtain quotes for the damage(s) before you decide whether to file. It does not make sense to file a claim if the damages are less than or just over your deductible.

NOTE: The questions asked to me will not go on your record.

As a reminder, all home claims and at fault accidents are subject to the deductible. This means the carrier will collect the deductible before anything is paid out.